The rapid onset of COVID-19 forever changed the e-commerce landscape. As shoppers switched from in-store to shopping online overnight, retailers had to revamp their supply chain strategy to accommodate higher volumes.

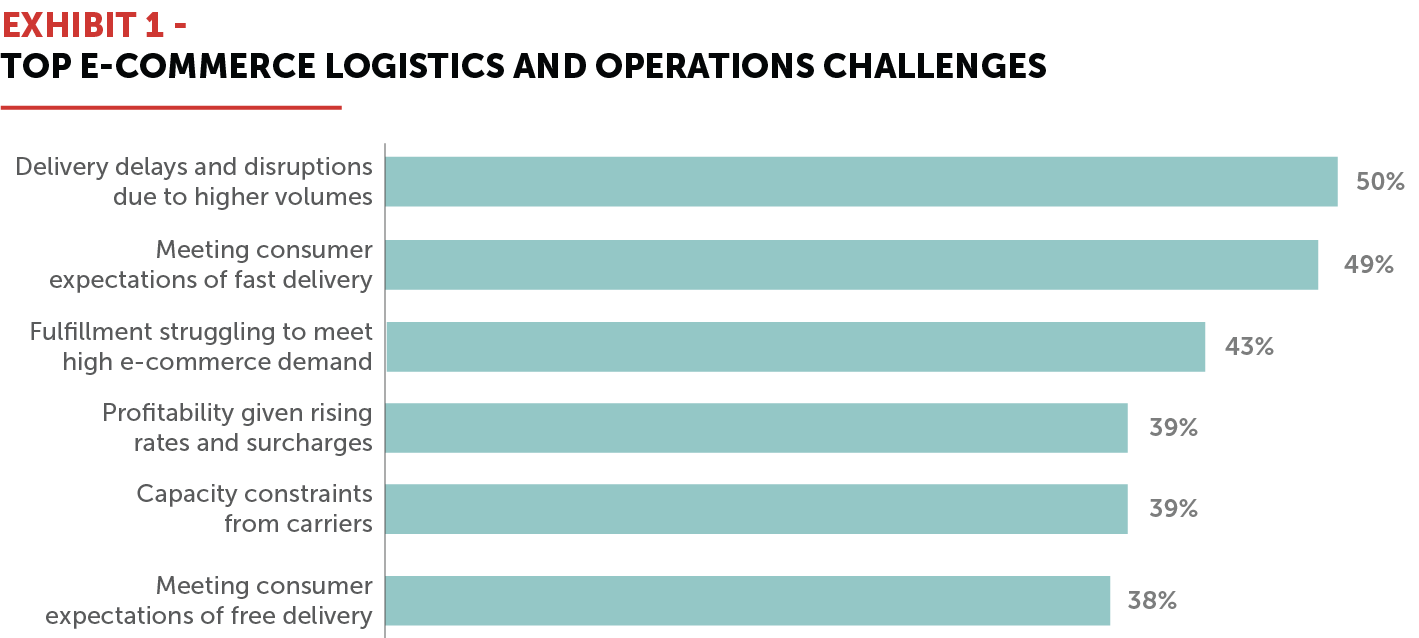

While the e-commerce shift has presented retailers with a number of growth opportunities, it has also created a number of logistics and operational challenges. Retailers are having to balance consumer demands of free and faster home delivery against rate increases, surcharges, and capacity constraints levied by national carriers. Exhibit 1 shows the top logistics and operational challenges supply chain professionals at large retailers are currently facing, including delivery delays, meeting consumer expectations of free and fast delivery, capacity constraints from national carriers, and rising rates and surcharges.

Accelerated levels of e-commerce show no sign of slowing down, and retailers need to adapt their supply chain strategies to meet evolving consumer expectations and overcome these challenges. LaserShip partnered with Hanover Research to survey over 100 C-Suite, VP, and director level supply chain professionals at large retailers who spend at least $50 million on parcel annually about the challenges they are currently facing, how they plan to respond to those challenges, and identifying areas where they plan to invest. The results indicate that national carriers are implementing more off-schedule rates increases, shipping volume is being capped, retailers have already implemented BOPIS and other forms of click and collect, faster delivery has become more important to consumers, and retailers are allocating more volume to regional carriers.

In this whitepaper, we will dive into the key takeaways and offer recommendations to help you overcome these challenges and position your retail business to gain an unfair share of the growing market.

Key Takeaways

-

Surcharges and Rate Increases Are Making Shipping More Expensive

-

National Carriers Are Capping Retailers’ Shipping Volumes

-

Retailers Have Already Implemented BOPIS and Click and Collect

-

Faster Delivery Has Become the New Free Shipping

-

Retailers are Allocating More Volume to Regional Carriers

Surcharges and Rate Increases Are Making Shipping More Expensive

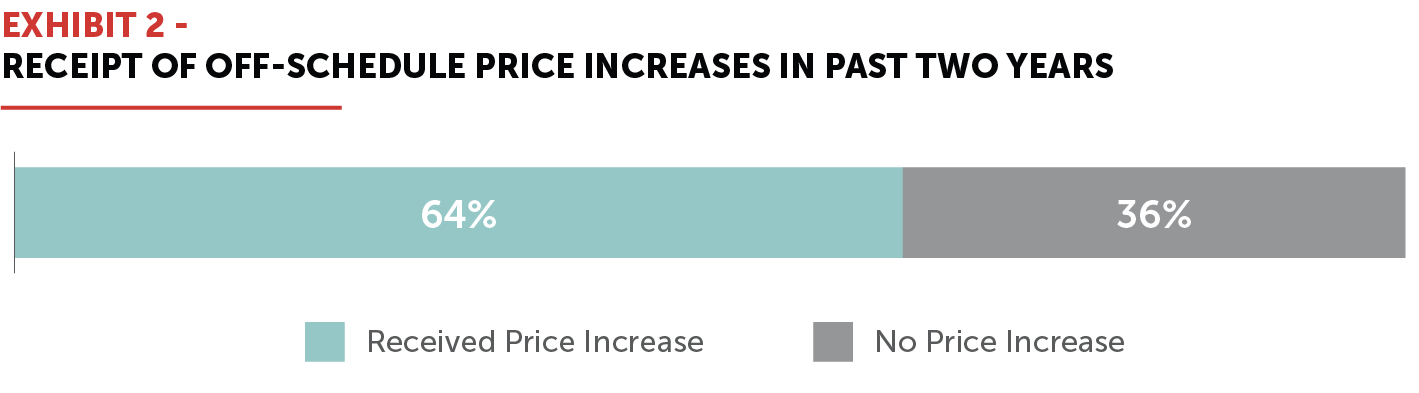

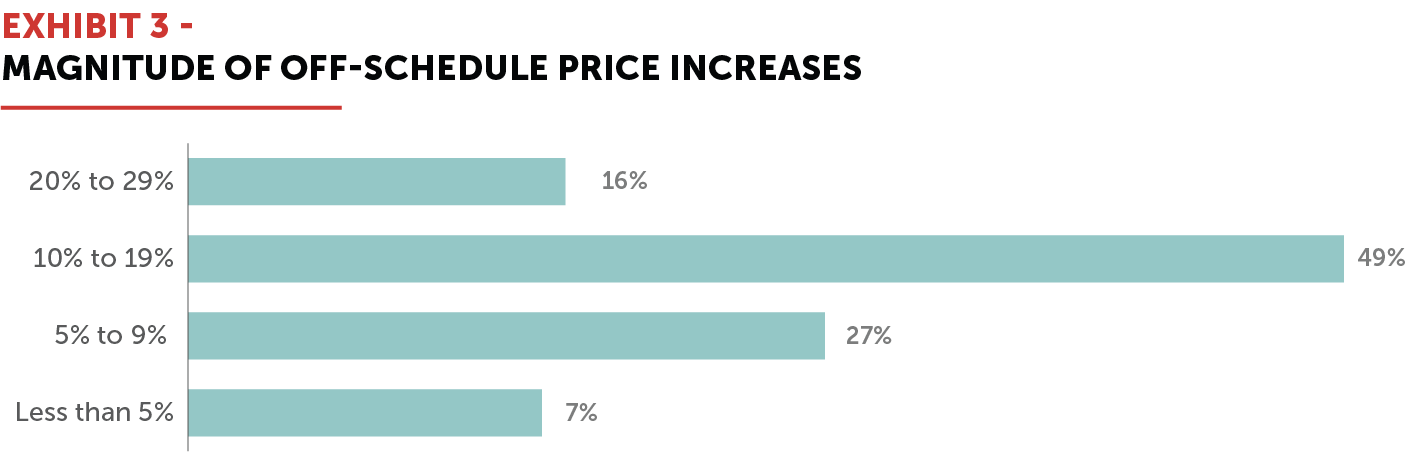

As online spending levels continue to increase, retailers are finding that working with FedEx and UPS is getting more and more expensive. Shipping rates are rising faster than they have in a decade, mounting the pressure on retailers to find ways to offset these soaring costs. Exhibit 2 shows that in the last 24 months, 64% of top online retailers have experienced an off-schedule price increase, in addition to general rate increases. Nearly half (49%) of these increases are price hikes between 10% and 19% and another quarter (27%) fall between 5% and 9% increases, as shown in Exhibit 3.

National carriers have been piling on surcharges and off-schedule cost increases since the beginning of the pandemic, and there is no end date in sight. FedEx announced a new set of parcel rate increases set to take effect in January 2022, which will raise the cost of its Express, Ground, and Home Delivery services by 5.9%. This marks the first time in nearly a decade that one of the major national carriers has strayed above annual increases of 4.9%. Raising prices in an environment where capacity is extremely tight, with no signs of letting up, necessitates that shippers look to alternative carriers to offset price increases, protect margins, and create flexibility within their supply chains.

National Carriers Are Capping Retailers’ Shipping Volumes

Before the pandemic, the United States domestic package market was projected to hit 100 million packages per day by 2026. That growth milestone is now expected to arrive in 2022, four years earlier than anticipated, with 86% of that growth expected to come from e-commerce.

This overwhelming growth has caused a major capacity crunch, and now hundreds of millions of packages are being capped annually. As shipping volumes continue to rise, national carriers have been imposing significant capacity limitations, putting retailers at serious risk of delays and disruptions. During the 2020 holiday shopping season, FedEx and UPS placed shipping limits on some of its largest retail customers.

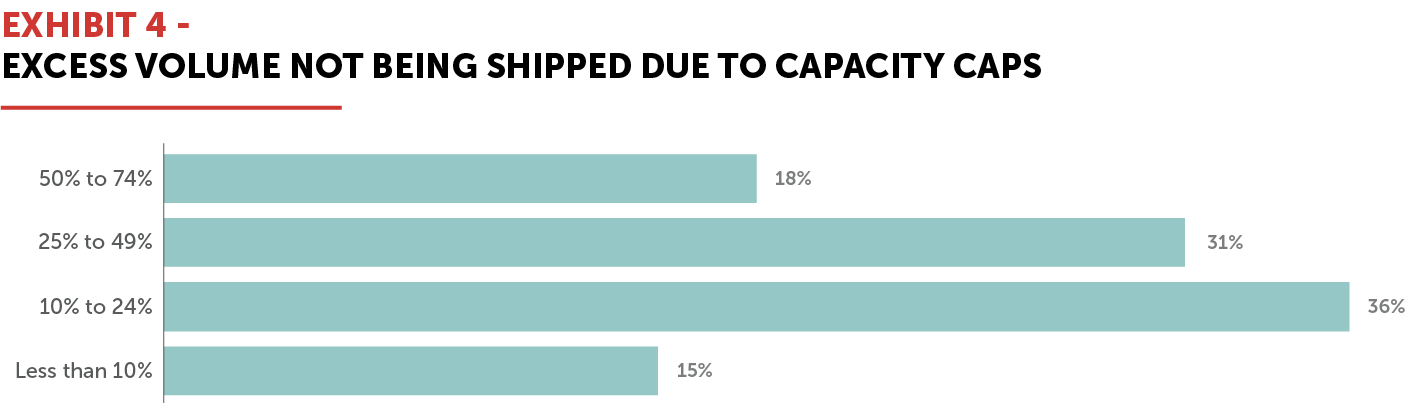

Thirty-four percent of retailers surveyed currently have their shipping capacity capped. Exhibit 4 shows that of those, two-thirds are facing caps between 10% and 49% of their total volume, resulting in an unprecedented capacity crunch with hundreds of millions of packages being capped annually

Capacity constraints are here for the foreseeable future, and retailers are feeling the impact heading into the holiday shopping season. When asked by Commerce Next about their logistics concerns for the 2020 holiday shopping season, retailers responded that the top two concerns were shippers capping deliveries during peak demand (60%) and shipper surcharges straining profitability (59%). With another busy holiday season ahead, these same concerns remain for 2021. UPS projects the package delivery demand during peak season to exceed the parcel market’s network capacity by 5 million packages per day, forcing retailers to look for other options or risk losing customers.

Retailers Have Already Implemented BOPIS and Click and Collect

In an effort to offset rising logistics and last-mile delivery costs, many retailers have implemented buy online, pick up in-store (BOPIS) and other forms of click and collect, including curbside pickup. According to FitForCommerce, 66% of retailers offered BOPIS at the end of 2019, but the adoption of BOPIS increased to 76% shortly after COVID-19 reached U.S. in 2020. Exhibit 5 shows that 87% of retailers surveyed are offering BOPIS from at least some store locations, while 85% are using ship-from-store.

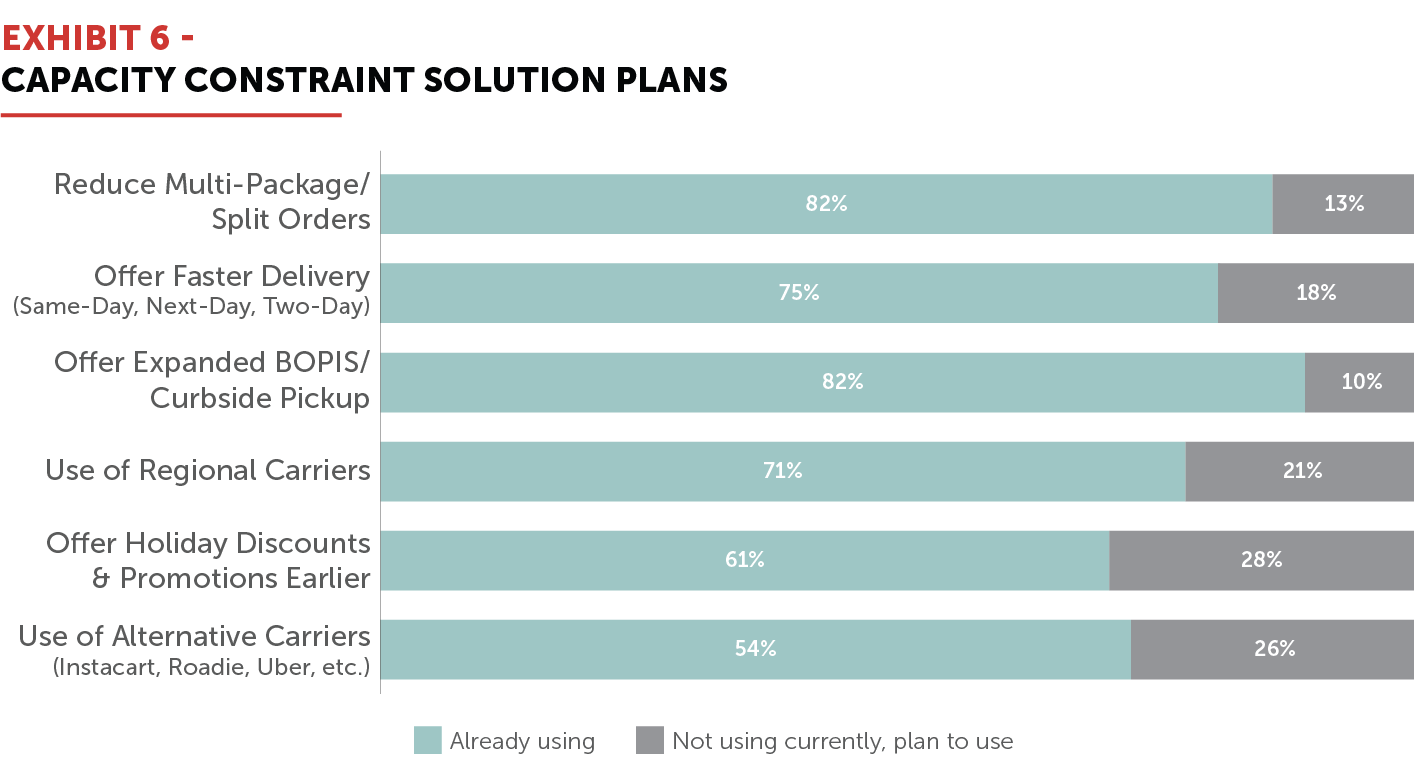

Retailers also identified BOPIS as the primary strategy to work around shipping capacity limitations implemented by national carriers. According to Exhibit 6, 54% of retailers plan to expand BOPIS and curbside pickup options.

In order to implement BOPIS successfully, retailers will need to make investments in inventory management systems to get real-time stocking updates and merge online and in-store inventory tracking. Retailers must also communicate clearly with customers across multiple channels on how to best use click and collect in stores to ensure an efficient, seamless pickup experience, while minimizing wait times. It remains to be seen whether or not the growth in click and collect adoption will continue after the pandemic.

Faster Delivery Has Become the New Free Shipping

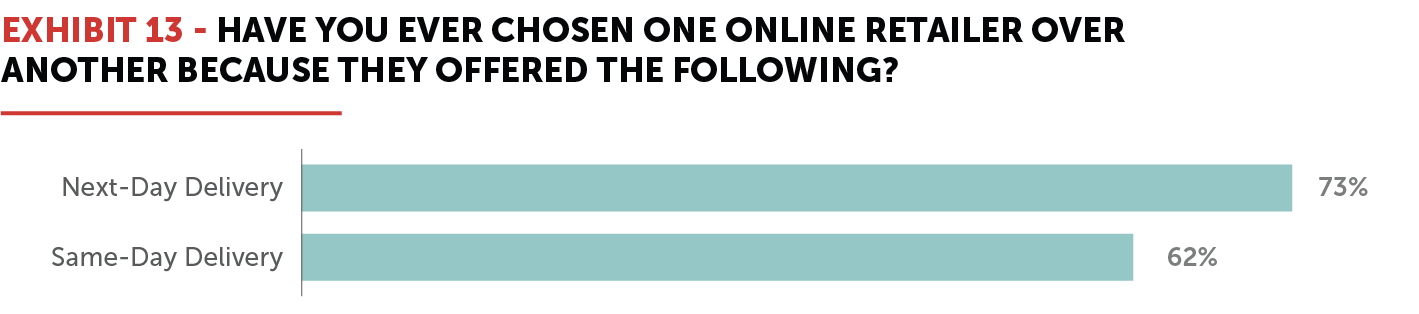

In today’s world of convenience and instant gratification, fast delivery is more important to consumers than ever. Shoppers gravitate to products and retailers specifically because expedited delivery is available, and slow delivery times drive them to shop elsewhere. We asked over 2,000 consumers about their online shopping habits and preferences, and 73% of shoppers surveyed chose one retailer over another because of next-day delivery options. Additionally, 64% reported that slow shipping caused them to switch retailers or prevented them from trying a new retailer.

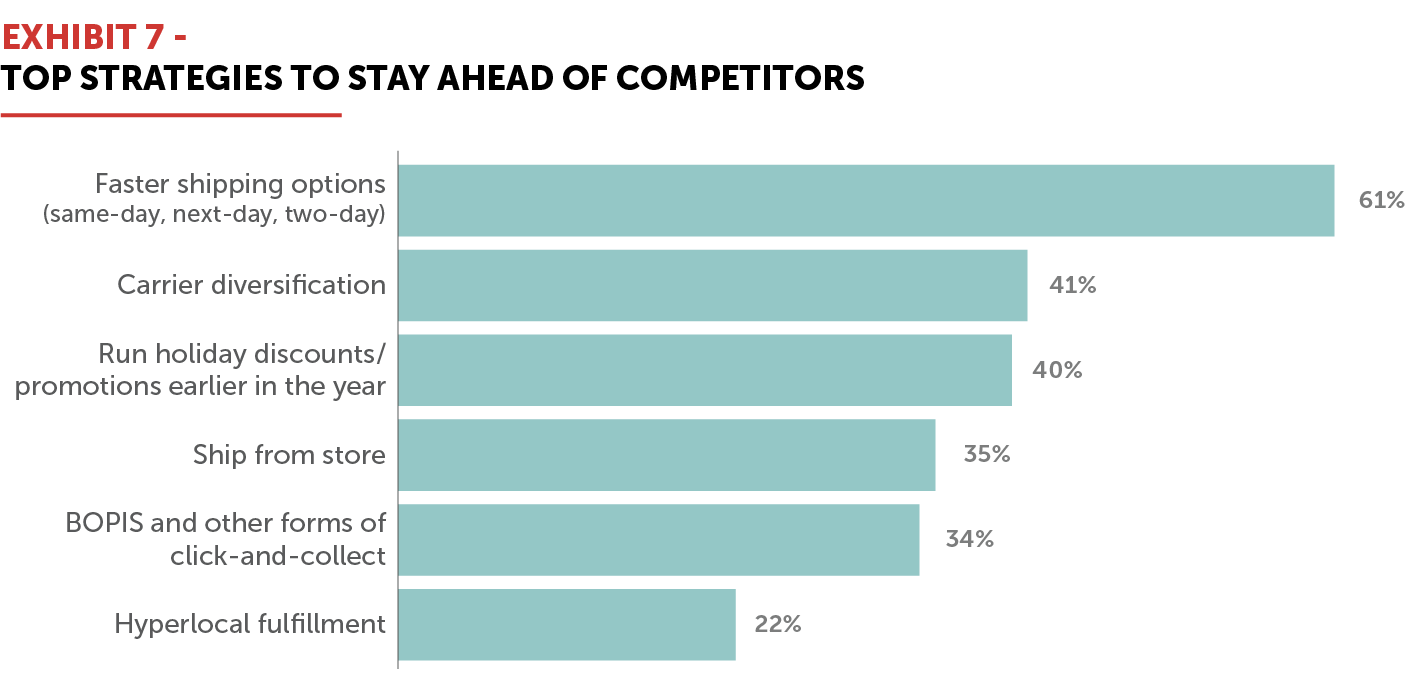

Retailers have taken note and are already working to build faster delivery into their supply chains. Exhibit 7 shows that 61% of retailers surveyed stated that offering faster shipping options is their primary differentiating strategy to stay ahead of the competition.

Retailers Are Allocating More Volume to Regional Carriers

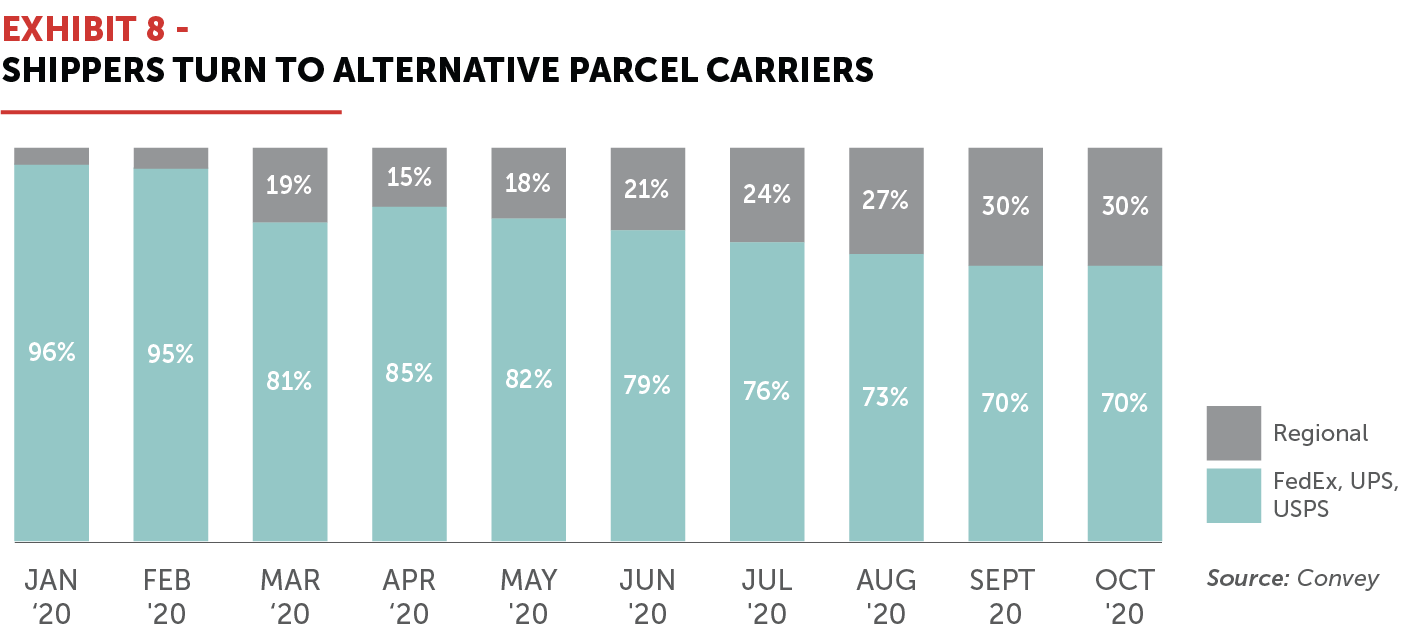

When the pandemic caused a shift from in-store retail to e-commerce in 2020, retailers were stuck after national carriers started imposing volume limits. As a result, retailers began shifting volume to regional carriers and many are still relying on regionals today to fill the void, as shown in Exhibit 8.

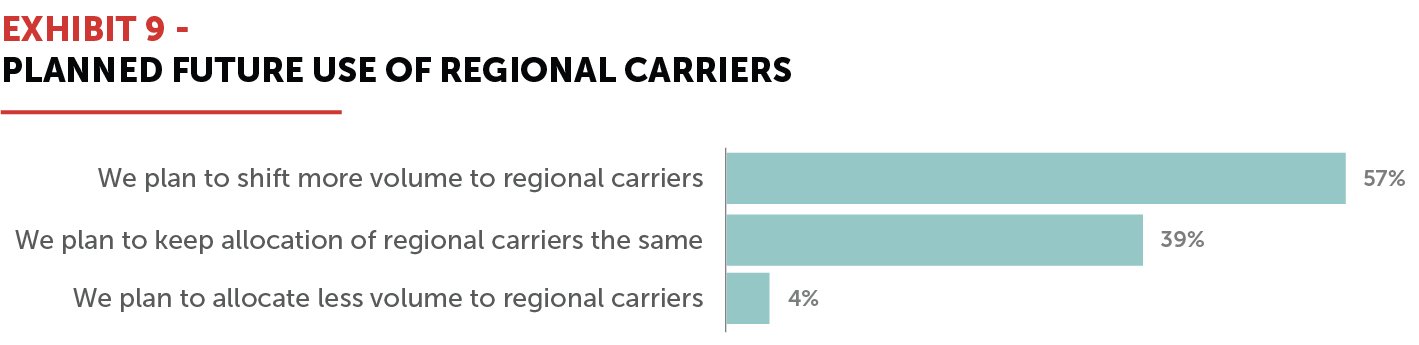

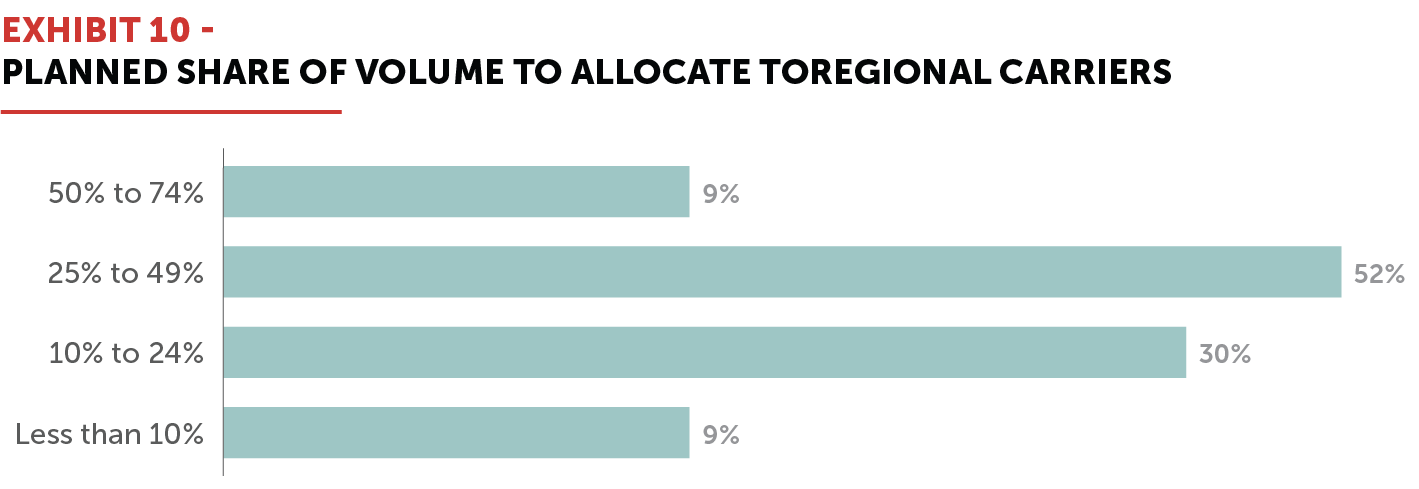

Regional carriers are a proven solution to the capacity constraints and cost increases being levied by national carriers. Retailers are aware of this and are adapting their supply chain strategies accordingly. Exhibit 9 shows that over half (57%) of major online retailers surveyed indicated that they plan to increase the volume shifted towards regional carriers in the future. Of those, 52% are planning to allocate between 25% to 49% of their volume to regional carriers, as shown in Exhibit 10.

Regional carriers offer faster delivery and more capacity, flexibility, cost-savings, and support than national carriers. With the majority of retailers planning to allocate more volume to regional carriers, retailers that do not do the same are at a competitive disadvantage.

How Can Retailers Adapt Their Supply Chain Strategies to Gain an Unfair Share of the Growing E-Commerce Market?

-

Build Faster Delivery into Your Supply Chain to Acquire Customers and Meet Their Expectations

-

BOPIS Is Not Enough to Offset Capacity Issues and Rising Rates–and It’s Creating a New Set of Challenges

-

Diversify Your Carrier Mix

Build Faster Delivery into Your Supply Chain to Acquire Customers and Meet Their Expectations

Much like free shipping, faster delivery has become table stakes and is no longer a “nice to have.” Shipping speed is critical to consumers’ decisions on where to shop, and retailers that can leverage faster shipping will gain a lasting competitive advantage.

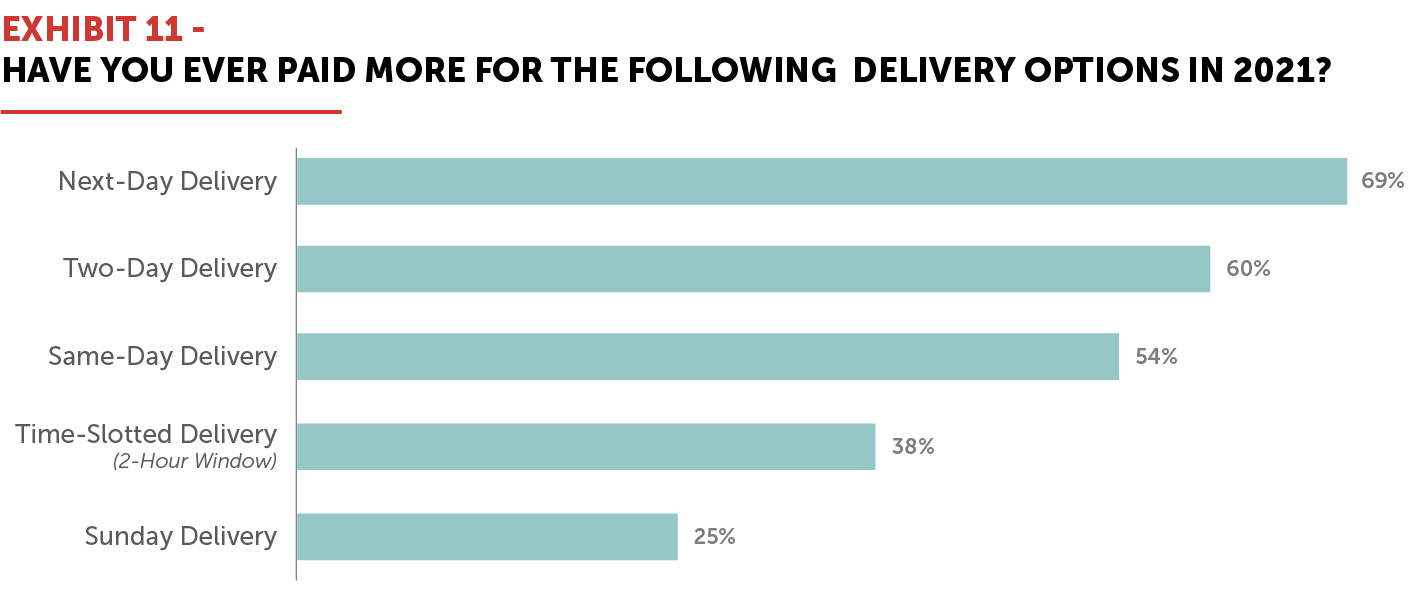

Faster delivery is a competitive differentiator for retailers, and consumers have made clear that they are willing to pay for it. 59% of shoppers surveyed stated that they have paid for faster delivery in 2021 alone, with 69% of those having paid more for next-day delivery, as shown in Exhibit 11.

Speed is especially important to Gen Z and Millennial consumers, who have grown up in the instant gratification era, and will increasingly drive purchase decisions as these younger generations expand their spending power. Retailers that can create easy, convenient shopping experiences with faster delivery options can establish relationships with young consumers early on and grow lifetime value in a competitive, brand-agnostic economy.

As reflected by the success of Amazon Prime, faster delivery can be used to acquire new customers and build brand loyalty. In fact, 78% of consumers surveyed would be willing to sign up for a loyalty program if it would mean faster deliveries. As shown in Exhibit 12 and Exhibit 13, the availability of next-day and same-day delivery has driven an overwhelming number of consumers to make a purchase or choose one online retailer over another.

COVID-19 called into question just how loyal consumers were to specific brands, leading retailers to look to redesign their loyalty programs to include more value-added services that consumers perceive as desirable. Fast and free delivery has become a common perk that brands are adding into their loyalty programs to increase customer lifetime value. To compete with Amazon, Walmart launched its subscription program, Walmart Plus, which includes same-day or next day delivery for specific items. Gap also updated its membership program to provide free and faster delivery to members that spend over a certain dollar amount each year.

When retailers accelerate how quickly they get items to their customers, they not only increase profits, but also take a larger share of the market. As more consumers shop online, retailers that can leverage faster delivery as a retention tool will increase customer lifetime value.

BOPIS Is Not Enough to Offset Capacity Issues and Rising Rates—and It’s Creating a New Set of Challenges

The number of consumers using BOPIS and other forms of click and collect has accelerated considerably since the start of the pandemic. However, the driving force behind consumers’ adoption of BOPIS is not convenience or preference—it is a direct result of retailers not having free and fast delivery options built into their supply chains. According to a Pew Research survey, 64% of consumers use BOPIS primarily to avoid paying shipping fees.

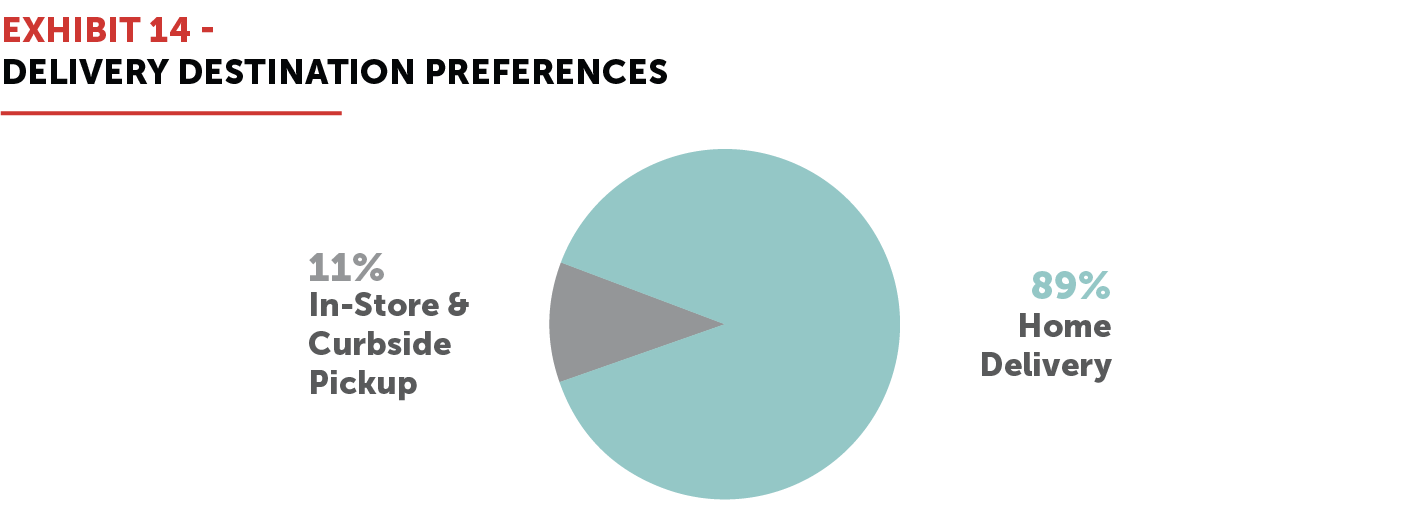

As a matter of fact, consumers still overwhelmingly prefer home delivery. Eighty-nine percent of shoppers surveyed indicated their preference for home delivery over BOPIS, as shown in Exhibit 14. Retailers should shift their focus from BOPIS to investing in supply chain solutions that meet consumers’ clear demands for convenience, speed, and reliability.

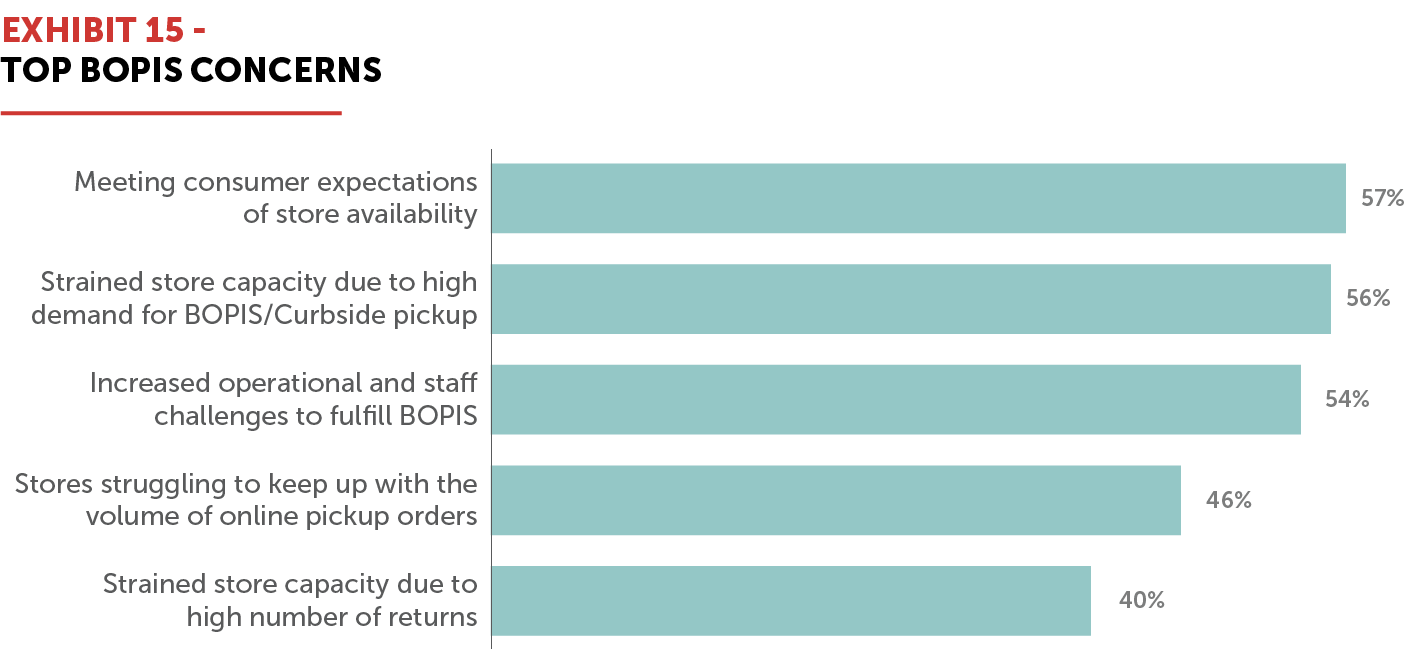

While there is no denying the growth of BOPIS, it also creates an additional set of operational challenges for retailers. Nearly all of the top online retailers are utilizing BOPIS, and yet major concerns remain around store availability and strained capacity, among other issues that largely stem from the physical stores themselves. 39% of retailers still view capacity constraints from national carriers as a top challenge they are currently facing. Ship-from-store has also proven problematic, with retailers noting increased operational and staff challenges as the top concern.

Retailers that do not offer free shipping are driving their customers to choose click and collect to avoid paying shipping fees. In turn, these retailers using BOPIS are plagued by logistics and inventory issues that put them at risk of losing customers. Consumers anticipate their BOPIS orders to be ready for pickup within a few hours after checkout. This expectation for a quick turnaround adds pressure to staff who may lack training in order fulfillment. Additionally, brick-and-mortar stores were not designed for fulfillment and pickup of online orders, and when inventory is not quickly available, retailers risk losing sales to competitors that can fulfill a consumers’ order more quickly.

BOPIS will continue to grow as another option for consumers, but it will not solve the excess capacity issues caused by shipping volume constraints from national carriers. As consumers increase their online shopping levels, retailers that can provide free shipping and deliver products directly to their customers’ doorsteps more quickly will build lifetime value and gain a significant edge over competitors, while also avoiding the additional operational problems and required investment that come with BOPIS.

Diversify Your Carrier Mix

Elevated levels of e-commerce have become the new normal, and the capacity crunch accelerated by the pandemic is not going away anytime soon. With more individuals shopping online, retailers need to adapt their shipping strategies to meet consumer expectations of fast and reliable delivery. Single-carrier shipping strategies have proven to be obsolete and can no longer support retailers’ growth moving forward. Retailers that diversify their carrier base can build flexibility and optionality within their supply chain, while avoiding surcharges and volume caps from national carriers that cause delays and risk losing customers. Compared to national carriers, regional carriers also have greater capacity, can deliver products to consumers faster and enhance the customer experience, and help retailers improve their margins with lower costs.

As evidenced by the off-schedule GRI increases and capacity constraints, national carriers have prioritized profits over relationships with their retail customers. The current environment is not just going to get better over time—these trends are here to stay for the foreseeable future. Relying on national carriers is a dangerous strategy that puts retailers at a competitive disadvantage, stunts growth, and causes them to lose money and customers. Retailers need to act now to aggressively remove themselves from the duopoly or lose customers and money.

The time to start looking to add regional carriers to your supply chain is NOW. With more retailers turning to regional carriers, it is important to be proactive and secure a regional carrier well in advance of peak season. Waiting until Q4 is too late, as most regionals have already planned for a certain amount of volume to deliver across their networks and will not be able to take on additional customers.

How Your Supply Chain Can Delivery Competitive Advantage

The e-commerce shift has created a number of positive opportunities, but as evidenced in the responses from top online retailers, the accompanying challenges of rising costs and capacity limits have had a significant impact on retailers’ growth. Tremendous opportunities exist for retailers that can adapt their supply chain strategy to overcome these challenges and meet consumer expectations. Retailers that can provide faster, more reliable home delivery and diversify their carrier mix to increase capacity and flexibility will differentiate themselves from competitors, gain an unfair share of the growing market, and build brand loyalty and lifetime value.

E-commerce shows no signs of slowing down, and retailers can’t afford to ignore the opportunity to offer faster, reliable delivery to acquire new customers, increase customer lifetime value, build supply chain flexibility and save money. Contact us to learn more about how last mile delivery can create competitive advantage for your business.

About the Author

Josh Dinneen is the Chief Commercial Officer at LaserShip, the leader in last-mile delivery and largest regional e-commerce parcel carrier in the U.S., where he oversees revenue strategy, sales, marketing, account management, and call center operations. Josh has over 18 years of experience in the industry, and prior to his current role, he created LaserShip’s e-commerce hub and spoke delivery network as the Vice President of Supply Chain.

About Hanover Research

Founded in 2003, Hanover Research is a global market research and analytics firm that delivers market intelligence through a unique, fixed-fee model to more than 1,000 clients. Headquartered in Arlington, Virginia, Hanover employs high-caliber market researchers, analysts, and account executives to provide a service that is revolutionary in its combination of flexibility and affordability. Hanover was named a Top 50 Market Research Firm by the American Marketing Association in 2015, 2016, 2017, and 2018, and has also been twice named a Washington Business Journal Fastest Growing Company. To learn more about Hanover Research, visit https://www.hanoverresearch.com.

Methodology

The findings in this report are based on a survey commissioned by LaserShip and conducted by Hanover Research of 114 supply chain professionals with decision-making power at large retailers who spend at least $50 million on parcel annually about the challenges they are currently facing. Percentages may not add up to 100% due to rounding. Some respondents chose not to answer certain demographic questions.

References:

- https://www.cnn.com/2021/09/20/business/fedex-shipping-price-increase/index.html

- https://www.wsj.com/articles/fedex-ups-rate-rises-are-making-online-shopping-more-expensive-11632173409

- https://www.dcvelocity.com/articles/51028-the-new-parcel-reality-record-volumes-tight-capacity-higher-costs-inconsistent-service

- https://www.wsj.com/articles/ups-slaps-shipping-limits-on-gap-nike-to-manage-e-commerce-surge-11606926669

- https://commercenext.com/how-will-covid-19-change-shopping-habits/

- https://www.supplychaindive.com/news/ups-earnings-peak-capacity-volume-carol-tome/603908/

- https://www.parcelpending.com/blog/reducing-shipping-costs-a-win-win-for-consumers-and-retailers/